MORS offers a comprehensive Asset Liability Management (ALM) and Treasury Management System (TMS). Designed for banks, our platform is built on an atomic architecture with a unified core, ensuring that whether you opt for individual modules or the entire suite, you leverage a holistic and seamless experience.

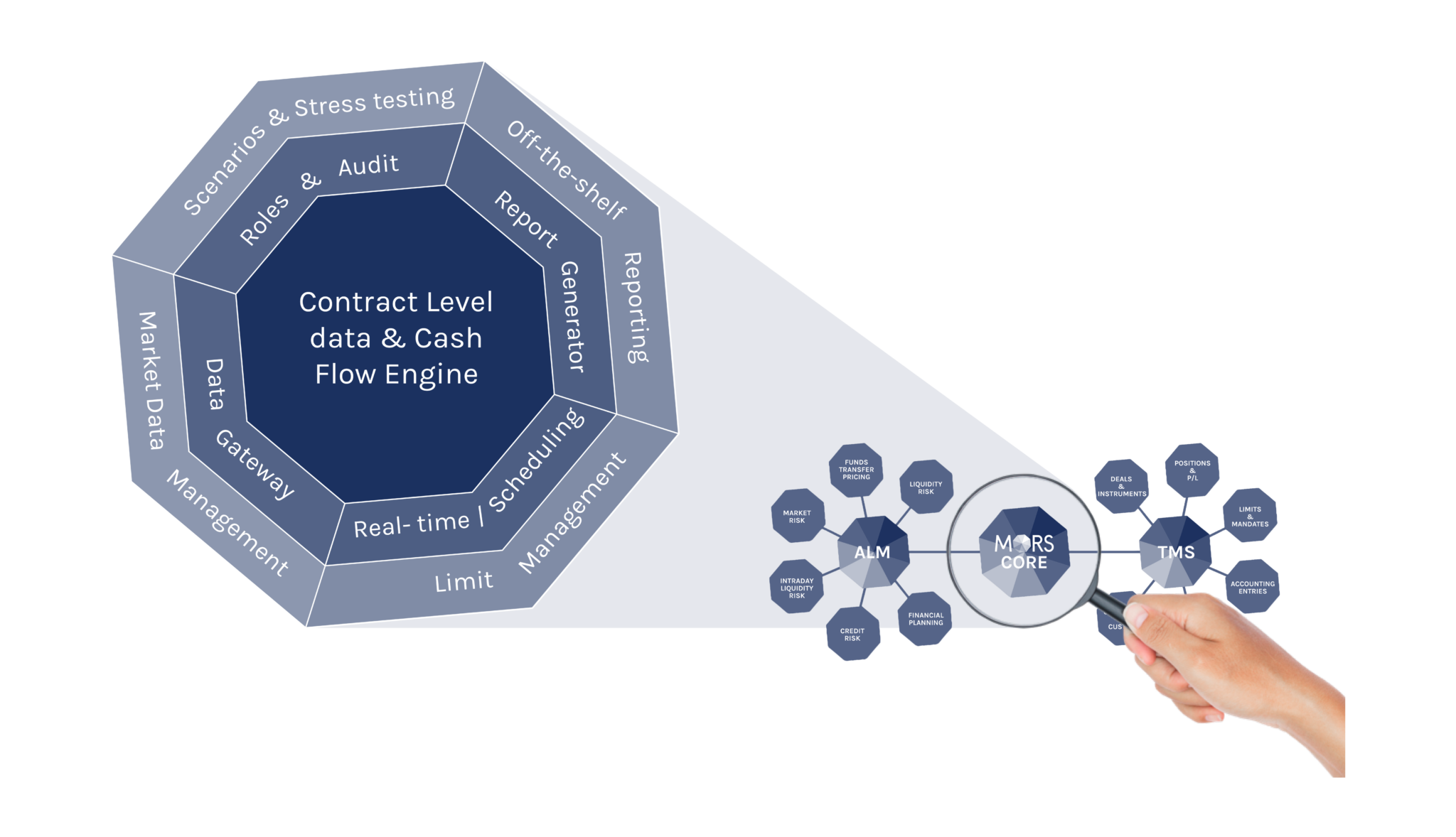

MORS is based on an atomic architecture centred around a common core of contract level data and common services. All functionality in this atomic structure is interconnected, providing a holistic system for optimising the performance and profitability of the bank at group and at entity level.

MORS supports complex group structures and the establishment and management of organisational models and respective Balance Sheet structures, creating a centralised and unified view of ALM and Risk management as well at individual entity level.

At a high level, MORS is made up of 2 distinct functional domains based on a common core, as depicted in the picture.

MORS Core is the central hub of MORS. It’s home to the data management layer, where contract level data is stored and managed for all products and instruments. It is also the home of Market Data which can be interfaced directly and automatically for all the market leading provider’s data subscriptions or internally from the bank.

MORS Core is also the place from which all central services and functionality is managed and then used by all modules of MORS. It takes care of many general administrative services such as user roles and permissions, audit trail, interfacing rules in and out of MORS. It also takes care of all scheduling matters for running processes, calculations, and reports either in real-time or on a periodic basis.

MORS Core provides configurable and flexible functionality for Stress Testing and Scenario Analysis applicable across all risk surfaces, Funds Transfer Pricing, and Limit Management. Virtual Modelling is provided for Deposit and Loan analytics, is highly configurable and can easily incorporate external models via a programmatic interface. MORS Core also provides a powerful built-in Cash Flow Engine for generating contracted and forecasted cash-flows. MORS Core is also where MORS manages Covered Bond Pools.

As an integral part of all aspects of MORS, both from a data perspective and functionally, MORS Core is the Engine Room of MORS. As such, MORS Core is the facilitator that ensures that MORS is truly atomic, and that all aspects of the solution work in a cohesive and holistic manner.

MORS delivers a complete, all-in-one solution that integrates Treasury and Asset Liability Management (ALM), tailored specifically for medium and small banks. Our system simplifies risk management by automating data management and minimising daily system maintenance, thereby reducing operational costs and enhancing efficiency. With MORS, you can enjoy the benefits of a holistic, integrated risk system that scales with your needs.

MORS offers large banks award-winning point solutions that solve individual risk surface requirements, such as IRRBB, Liquidity Risk Management, and Intraday Liquidity Risk, to name but a few. These solutions are not only tailored to the unique challenges faced by larger financial institutions but are also recognised for their sophistication and excellence. By leveraging MORS’s cutting-edge analytics and real-time data processing, banks can not only meet regulatory demands but also gain a competitive edge through enhanced decision-making and strategic planning.

MORS allows you to do the right thing, in the right way, at the right time. This means you can focus on the material risks, as MORS delivers the required and timely information to make the right decision. The MORS System operates in real or near real-time, further enhancing your ability to respond swiftly and effectively. By choosing MORS, you partner with a vendor that’s committed to making your operations smoother, your life easier and enabling you to optimise your risk reward ratio.

The only risk management System for banks offering Asset Liability (ALM) and Treasury Management (TMS) truly in one box. Depending on your priorities and requirements, you have the flexibility to purchase either the full solution or one module. Discover how MORS can transform your Treasury and ALM by visiting each module’s detailed page.

ALM software for banks that covers Financial Risk Management for Market, Liquidity and Credit Risk. Fully fledged profitability and performance forecasting.

MORS Treasury Management System (TMS) offers comprehensive treasury management for the first, second and third line of defense, integrating deal capture, position keeping, reporting and trade processing.