ALM software for banks that covers Financial Risk Management for Interest Rate, Liquidity and Credit Risk. Fully fledged profitability and performance forecasting.

MORS Asset Liability Management Software for banks, is an award winning solution that covers Financial Risk Management for Interest rate, Liquidity Risk and Credit Risk. It also offers fully fledged profitability and performance forecasting. While MORS is available as one integrated asset liability management system, it is also available as a point solutions.

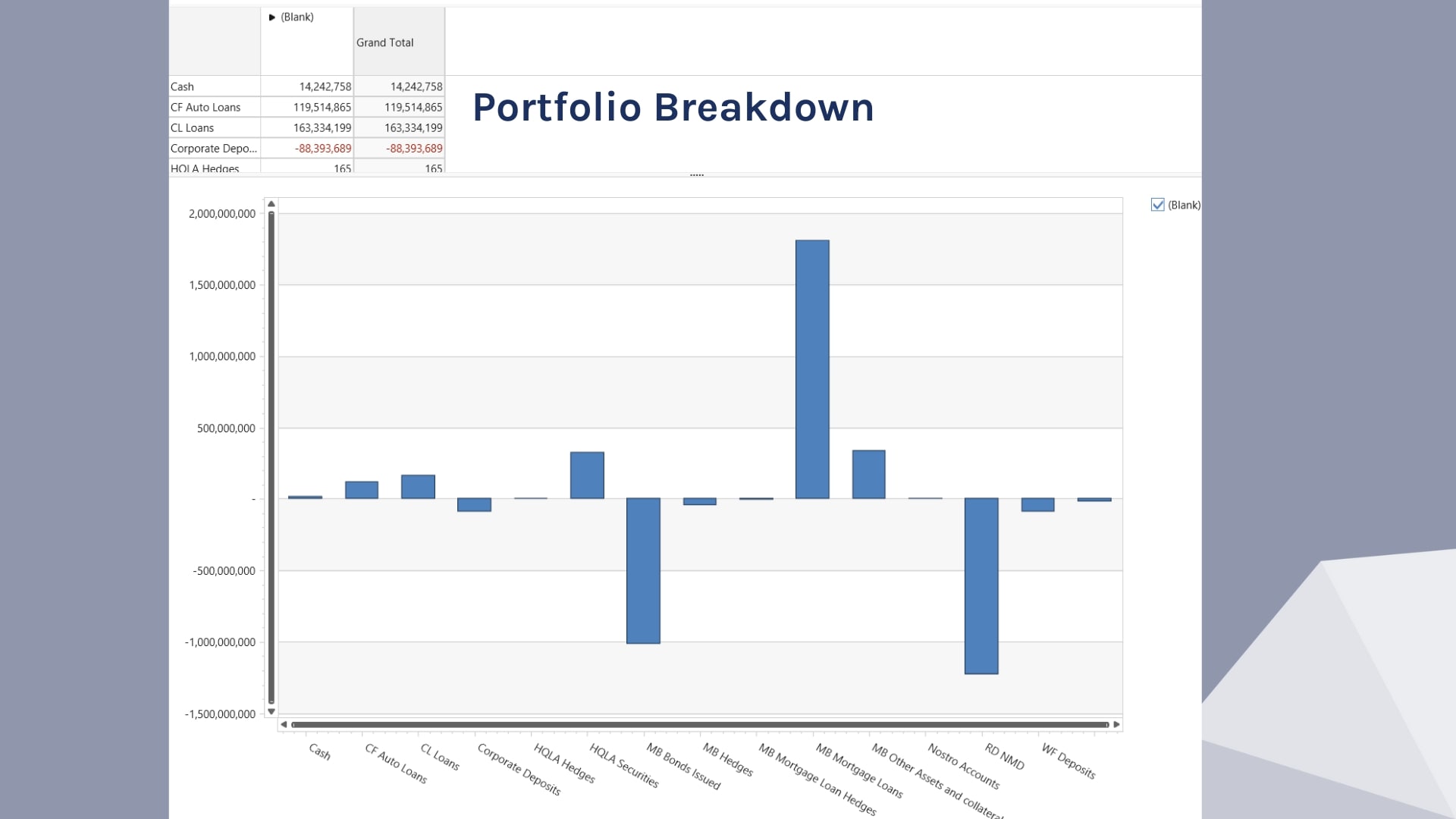

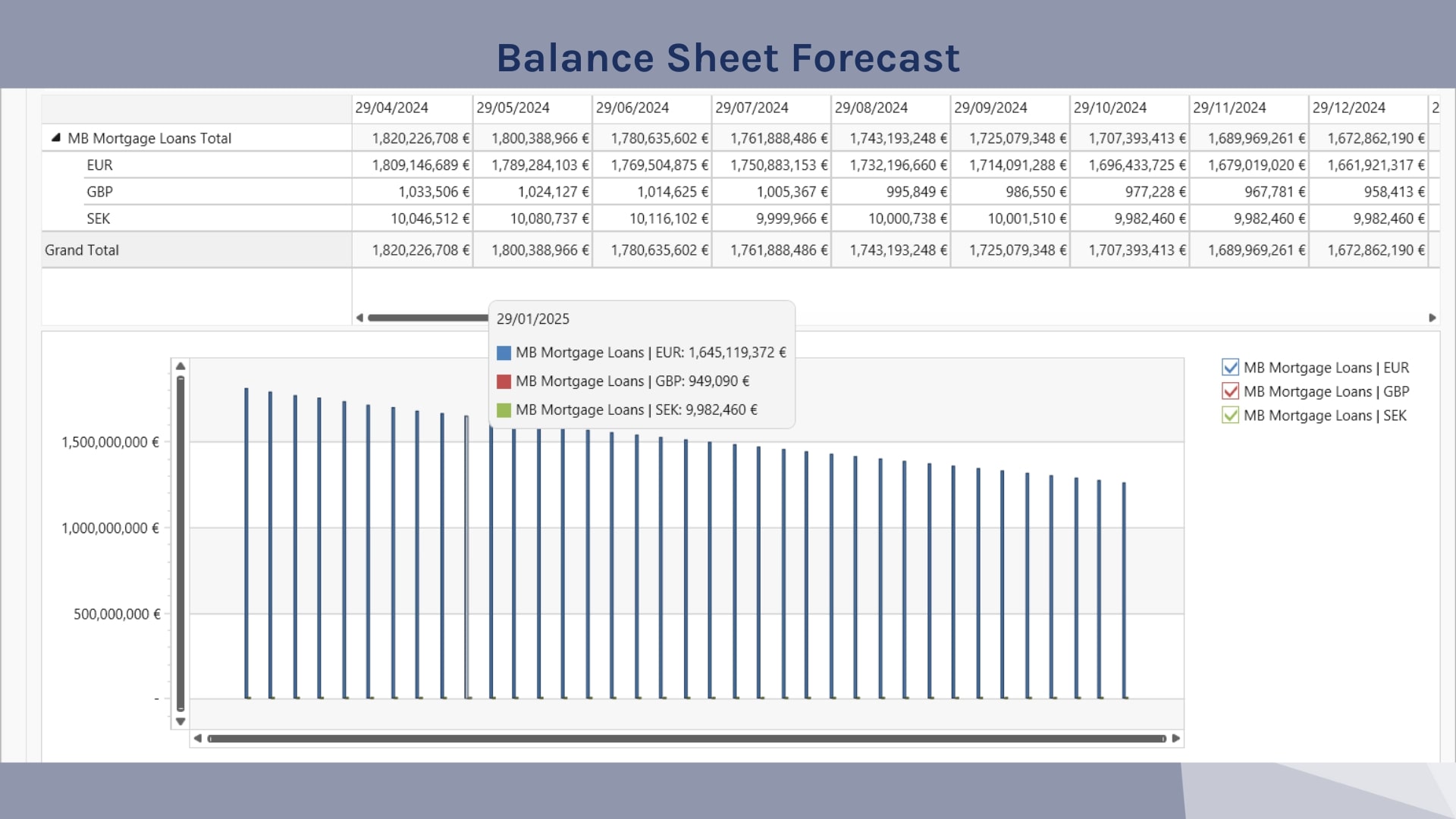

Balance sheet imported into MORS on single deal level, providing excellent data lineage and superb analysis from a top of the house view to single deal and single cashflow analysis.

Largely automated data management which will heavily reduce operational costs normally associated with Asset Liability Management systems.

Real-time time system always providing up to date reporting and the ability to generate new scenarios on the fly, even for heavy calculations such as Net Interest Income forecasts.

Superb Visualization tools especially for use at for example board level and ALCO meetings, providing excellent key decision support.

Especially for small and medium sized entities, using MORS Treasury Management System (TMS) as an add on to MORS Asset Liability Management makes perfect sense, providing one holistic and integrated system, without the operational hassle and cost of operating two separate systems

MORS Asset Liability Management offers comprehensive Financial Risk Management across all risk surfaces. Financial risks are covered both from prudential and from internal risk management points of view.

MORS covers an extensive set of market risks. These include Interest Rate Risk in the Banking Book (IRRBB) from an Economic Value of Equity (EVE) and from an Earnings at Risk (EaR) points of view. Related to IRRBB, MORS covers Gap, Basis and Option Risk. It should be noted that MORS can be used seamlessly for Interest Rate Risk management both for day to day or operational IR Risk management and for scenario type risk management. Offering a transparent rules engine, the user can easily modify, copy & paste or create new scenarios from scratch.

An off the shelf and very fast historic Value at Risk (VaR) analysis is provided as part of the Market Risk repertoire.

FX risk analysis is available both as specific and tailored FX analysis, as well as across all reports which can be broken down by currency or consolidated into base currency.

MORS Liquidity Risk covers both Liquidity and Intraday Liquidity Risk Management.

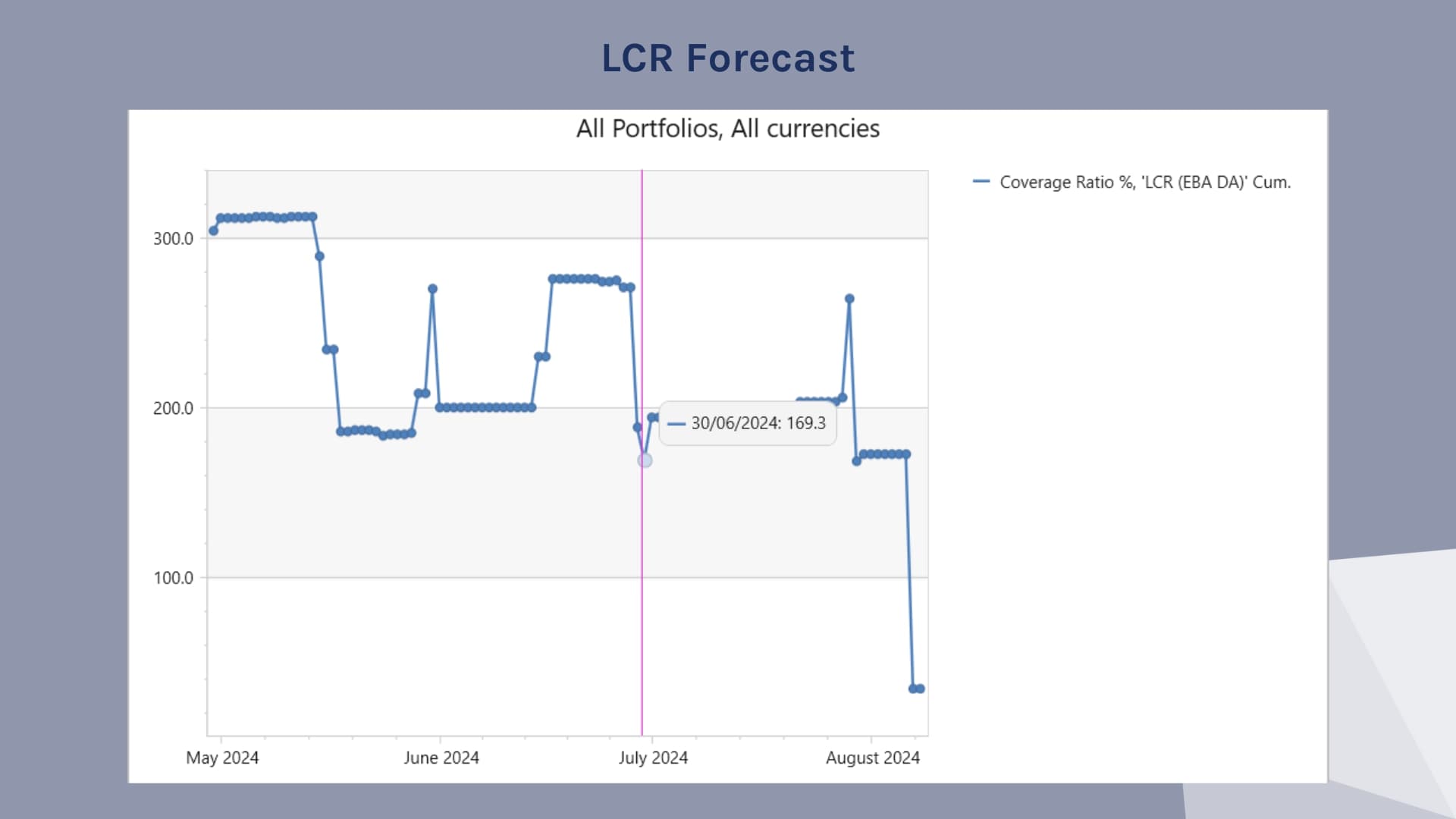

With MORS, it is easy to measure key Liquidity Risk Indicators such as the LCR, NSFR and Survival Horizon in real-time or near-time. MORS also provides liquidity ladder style reporting, meaning calculations such as the Additional Liquidity Monitoring Metrics (ALMM) are supported.

The MORS rule engine allows a broad range of scenarios to be set up, both regulatory scenarios and scenarios for internal use. In the scenario definition, the user can for example define inflow and outflow assumptions, as well as assumptions for the liquid asset buffer.

Forecasts for ratios are fully supported as well as historical analysis of key ratios and their components.

MORS supports Intraday Liquidity Risk Management both for regulatory purposes, for operative intra-daily cash management, as well as for forecasting liquidity in the next business days. Nostro account balances and payments can be imported from Swift messages (MT and Camt formats). MORS also supports IBM MQ messages. Finally, Open Banking style APIs are also an option for importing account balances and payments. A comprehensive set of reports for intraday analysis is included. These cover both the historical angle, as well as forward looking analysis.

MORS offers Credit Risk features primarily for Expected Credit Loss (ECL) calculations and for Counterparty Credit Risk (CCR) management.

ECL in MORS is heavily focused around income forecasting, i.e., forward looking earnings projections with ECL as one of the key components in the projections. For the ECL calculations and forecasts, MORS offers flexible ways of importing or entering key variables, such as Probabilities of Default (PD) and Loss Given Defaults (LGD)

MORS Counterparty Credit Risk functionality allows banks to set up almost any type of Counterparty, including single counterparty, groups / segments, countries, sectors, etc. The Limit classes are also fully configurable and can for example be set up as, settlement, short term, long term and Equity / Capital Limits. All of the exposures versus limits can be monitored in real-time, allowing for full drill down of a consolidated exposure, to a single deal and counterparty exposure.

MORS offers our clients unparalleled support for profitability and performance management purposes, covering balance sheet management, financial planning, capital planning and funds transfer pricing accordingly.

MORS is an award-winning balance sheet management solution, based on our unique transaction-based integration, providing a consistent view across all risk surfaces.

The powerful scenario engine, combined with in-memory analytics and virtual modelling, enable our clients to manage their financial resources in real-time.

With complexity and multi-dimensional interaction between risk drivers and financial constraints, good scenario analysis capability and the possibility to visualise online different outcomes and how they impact profitability is paramount – MORS supports our clients in optimising their financial resources.

MORS award-winning balance sheet management solution allows banks to cross the bridge from balance sheet to income statement alike. Profitability drivers can be analysed, the impact on financial constraints measured, as banks are able to understand the impact and correlation between net commissions / provisions and net interest income.

Real-time visualisation further enhances the offering, as decision-makers can understand the potential implications of their decisions online.

The sensitivity to all material risk drivers, is incorporated, with the ability to simulate online how different KPI’s, financial resources and profitability would evolve under different stressed scenarios.

Real-time earnings forecasting and scenario analysis, combined with loan loss provisioning support and the ability to incorporate net commissions, as part of the integrated income statement forecast in MORS, are some of the key features that support banks as part of their capital planning process.

Online stress-testing capabilities, combined with ability to utilise the powerful visualisation layer further enhances the offering.

MORS offers a comprehensive Asset Liability Management (ALM) and Treasury Management System (TMS). Designed for banks, our platform is built on an atomic architecture with a unified core, ensuring that whether you opt for individual modules or the entire suite, you leverage a holistic and seamless experience.