Complete Asset Liability Management (ALM), Risk Management and Treasury Management Solutions (TMS) for banks.

MORS makes it easy for banks to grow. Regulatory requirements and financial risks shouldn’t hold banks back.

We enable your bank to scale, add new products and to manage risks.

Features - MORS Solution

The only risk management System for banks offering Asset Liability (ALM) and Treasury Management (TMS) truly in one box. Depending on your priorities and requirements, you have the flexibility to purchase either the full solution or one module. Discover how MORS can transform your Treasury and ALM by visiting each module’s detailed page.

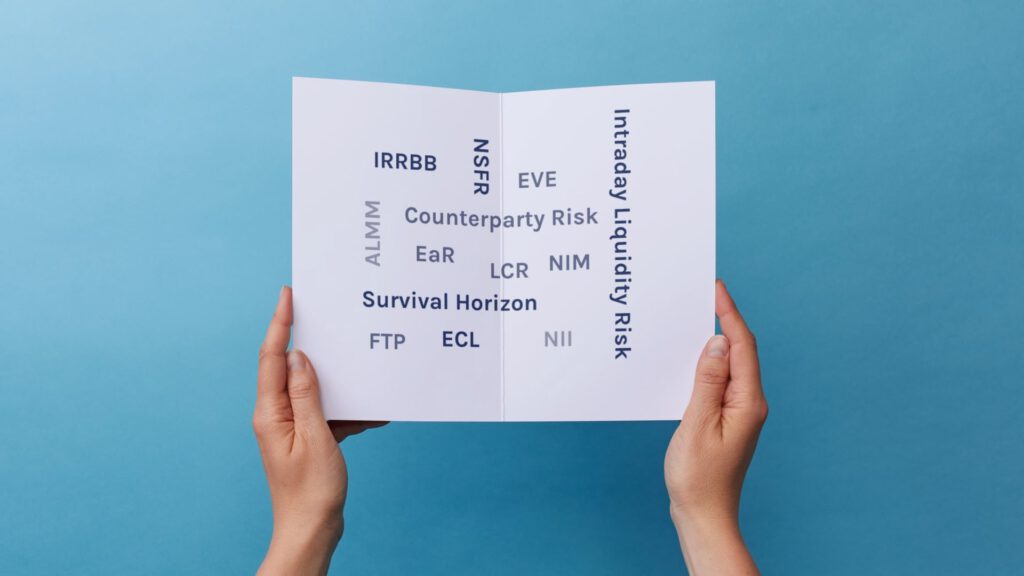

ALM software for banks that covers Financial Risk Management for Market, Liquidity and Credit Risk. Fully fledged profitability and performance forecasting.

MORS Treasury Management System (TMS) offers comprehensive treasury management for the first, second and third line of defense, integrating deal capture, position keeping, reporting and trade processing.

At MORS, our Finnish ethos of sisu—persistence, determination, and practicality—guides our approach to every project. We don’t waste your or our time. And we’re known for our swift and efficient implementations, typically completed within 4 to 8 months, and a direct, honest communication style that ensures minimal fuss and low project risk. Our standardised implementation approach ensures a seamless setup, maximizing value from day one. We offer implementation projects at a fixed price, ensuring there are no cost surprises.

All-in-one Treasury and ALM Solution for Medium & Small Banks

MORS delivers a complete, all-in-one solution that integrates Treasury and Asset Liability Management (ALM), tailored specifically for medium and small banks. Our system simplifies risk management by automating data management and minimising daily system maintenance, thereby reducing operational costs and enhancing efficiency. With MORS, you can enjoy the benefits of a holistic, integrated risk system that scales with your needs.

Advanced Point Solutions for Large Banks

MORS offers large banks award-winning point solutions that solve individual risk surface requirements, such as IRRBB, Liquidity Risk Management, and Intraday Liquidity Risk, to name but a few. These solutions are not only tailored to the unique challenges faced by larger financial institutions but are also recognised for their sophistication and excellence. By leveraging MORS’s cutting-edge analytics and real-time data processing, banks can not only meet regulatory demands but also gain a competitive edge through enhanced decision-making and strategic planning.

Do the right thing, in the right way, at the right time

MORS allows you to do the right thing, in the right way, at the right time. This means you can focus on the material risks, as MORS delivers the required and timely information to make the right decision. The MORS System operates in real or near real-time, further enhancing your ability to respond swiftly and effectively. By choosing MORS, you partner with a vendor that’s committed to making your operations smoother, your life easier and enabling you to optimise your risk reward ratio.